Headline economics and its recursive logic

Prices can revert to the mean. Capital allocations often can't.

Last Sunday, a researcher and fellow Substack writer Citrini posted a question on X. It began in the future tense: June 2028. The S&P had plunged 38% from its peak. Unemployment clocked in at 10.2%. AI had not only met expectations, it had shattered them. What happened?

The thread linked to a full article. Twelve thousand words of speculative macro fiction of AI agents replacing half the white-collar workforce, private credit unraveling, prime mortgages cracking in tech hubs, a deflationary spiral no one modeled because the cause wasn’t failure but success. It was a thought exercise, from the future. Citrini said.

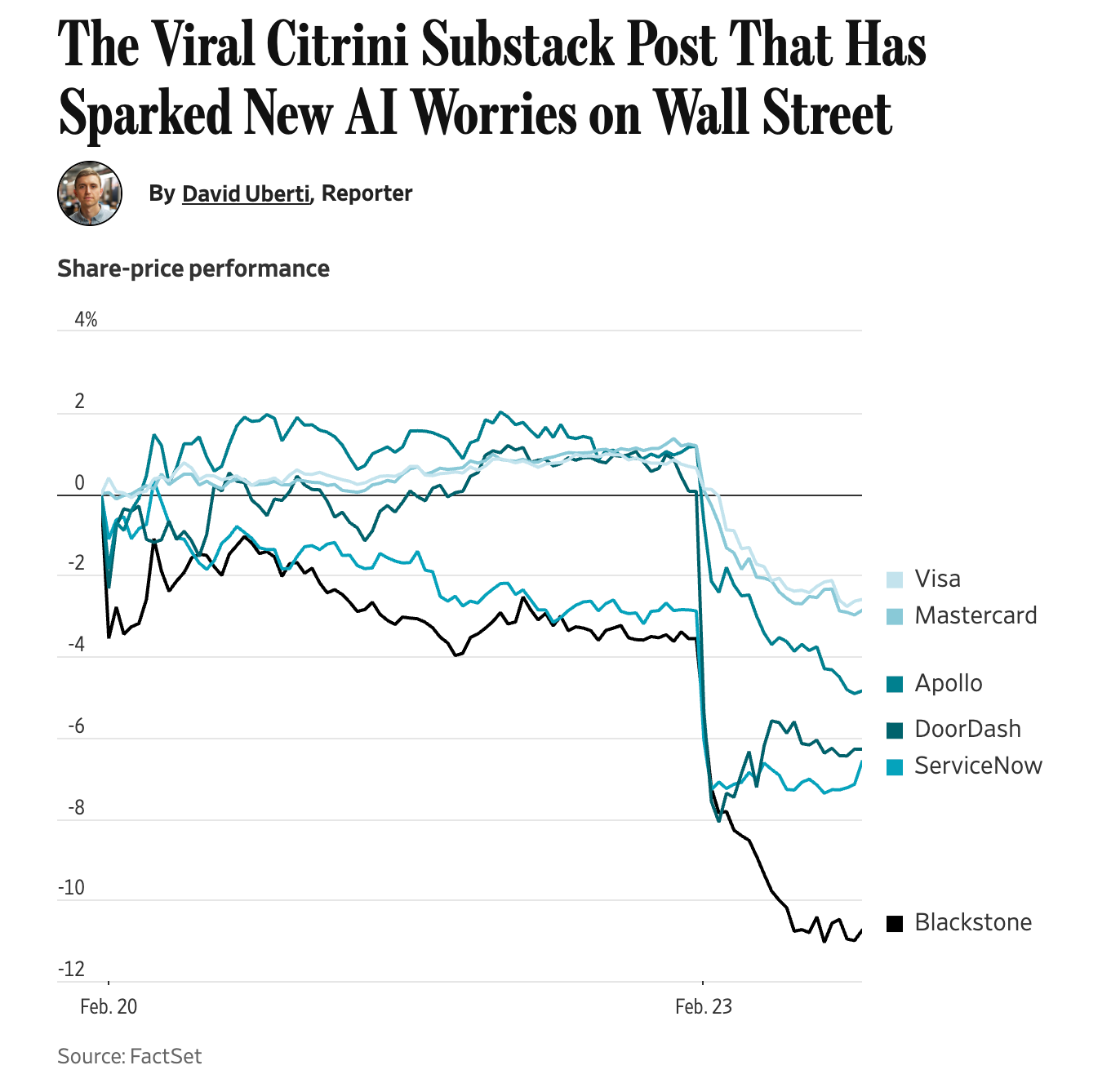

Twenty-one million people read the post, and forty-four thousand bookmarked it. Investors around the world copy and paste the post into their ChatGPT (paid by their employer) and ask: Stress test my positions against this thesis, assuming it’s ALL TRUE.

When markets opened Monday morning, DoorDash tumbled 8%. American Express followed suit. Apollo, Blackstone, Visa, Mastercard, ServiceNow. Every company named in the thought experiment—dropped between three and eight percent. The iShares software ETF hovered near a 52-week low and wiping out nearly all the gains since ChatGPT’s debut in November 2022. Three years of the AI trade, erased before lunch. Bloomberg and The Wall Street Journal both ran with the story, pinning the selloff on a Substack post. All this, triggered by a piece of fiction, openly labeled as such, penned by a researcher unknown to most of Wall Street.

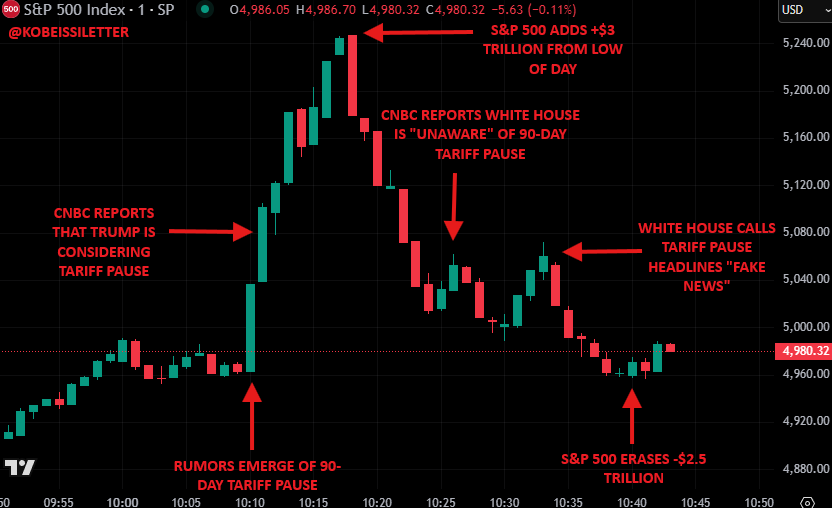

Ten months earlier. April 7th, 2025. An account called Walter Bloomberg (not affiliated with Bloomberg), just a dude with a blue checkmark and a propensity of posting headlines in all caps, writes: HASSETT: TRUMP IS CONSIDERING A 90-DAY PAUSE IN TARIFFS FOR ALL COUNTRIES EXCEPT CHINA.

It wasn’t true. Kevin Hassett had been asked about a pause on Fox News that morning and given the kind of non-answer that is, in Washington, a form of silence. “I think the president is going to decide what the president is going to decide.”

But the headline had already escaped. CNBC read it live. Reuters published it. In just ten minutes, from 10:08 to 10:18 a.m., the S&P soared 8%. Two point four trillion dollars moved. The White House called it fake. Walter Bloomberg deleted the post. Reuters retracted. Stocks crashed 3.5%. Ten minutes. A misquote of a non-answer, launched by a man playing news wire.

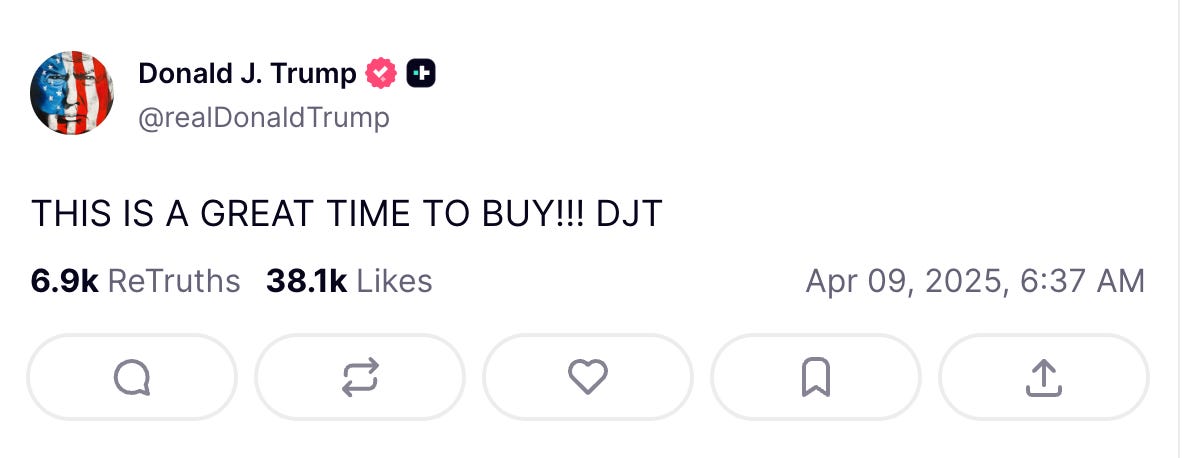

Two days later, Trump actually paused the tariffs. For ninety days. Exactly as the fake headline had described. But hours before announcing the real pause — the one that would add four trillion dollars back to the market — he posted on Truth Social, also in all caps: THIS IS A GREAT TIME TO BUY!!! DJT.

The fake headline seems to have predicted the real policy. The real policy was announced via social media post. The president told people to buy before the announcement. Lawyers said it would trigger an investigation in any other administration. The Commerce Secretary later said he had been in the room while the president typed it.

And then October. A single Truth Social post, “massive increase” in tariffs on China, erased more than hundreds of billions from U.S. semi stocks market cap in a day. Trade deals were announced, tweaked, scrapped, and revived, all through social media, all at the speed of a keystroke, long before the machinery of government could even open a Google Doc.

What once demanded a Soros is now open to any theorycel with a Substack. A researcher posts a scenario and the scenario shapes the sector, at least the perception of it. A blue checkmark posts a headline and the headline becomes policy. It’s called alpha launch, but for a headline. Soros’ reflexive loop is now compressed, democratized, stripped of the institutional drag that once gave people time to think. We’ve evolved past his framework. The loop no longer needs to be understood to work. It no longer requires meaning. It only needs motion.

This is headline economics, and its logic recursive.

The Carcass

Yorgos Lanthimos’s new film Bugonia tells the story of a kidnapping that also serves as a test of what we know and believe. A man kidnaps a female CEO because he thinks her company is killing the bees and his mother, and that she is an alien following orders from an emperor in Andromeda. He turns out to be right about everything. Still, Lanthimos, who might be the cruelest filmmaker working today, makes sure that this truth does not change anything.

The conspiracy theorist has the facts. His accuracy is beside the point. What his pain requires is not truth but form — a villain, a structure, an address to which suffering can be sent. Without one, pain is ambient and therefore permanent. Conspiracy cognition is compensatory agency. It restores the feeling of participation in a system that has locked you out of every lever.

The CEO inhabits the opposite epistemology. She does not need to deceive because the logic of corporate game theory has become the architecture of her cognition “My company is a key job creator and economic engine of the region. I am crucial.” No irony. She has produced a measurement framework so internally coherent that outside perspectives are rendered not wrong but unintelligible. She doesn’t see what he sees, because her instruments were calibrated for a different set of heuristics entirely.

The film’s title comes from Virgil. Bugonia is the old belief that bees are born from the body of a sacrificed ox. It is the idea of life coming from decay, sweetness from death. In truth, what actually came out of the ox were drone flies, colored black and gold, fast enough to look like honey bees. Virgil might not have known the entomology, but he understood human nature. The myth is not about facts, but about wanting something so badly that a person will see a fly and call it a bee, because facing the truth—that the ox died for nothing, that sweetness will never come, that decay is just decay—is too hard.

The fact that the fly looks like a bee is not a mistake; it is central to how the system works. The market does not just reflect reality, it creates it when needed. The K-shaped split in the economy does not only lead to different results, but also to different stories people need to tell themselves. These needs are so different that they create worldviews that cannot be reconciled, each making sense on its own but impossible for the other side to see.

The theorist’s paranoia creates a villain and a story that keeps his fears going. The executive’s power depends on order, so she creates the numbers that support her position. When these two ways of thinking clash, it does not mean the economy is broken. Instead, it shows the design of a new system. This system runs on people who can turn flies into bees in their minds. The strange thing is, if enough people believe it, the illusion continues.

The system still makes honey.

Shiller almost described it, and Soros came even closer, but neither fully captured what happens once latency tends to zero. Soros’s reflexive loop implies that the cognitive function has time to update before the manipulative function finishes its work. In headline economics, that order reverses, where the manipulative function races ahead of cognition. By the time anyone has processed the claim, the trades have already detonated across a levered system.

Reflexivity doesn’t unfurl as a loop that can be ampped but arrives as an explosion whose shockwave redraws the landscape that has yet to be understood.

When latency approaches 0

Trying to focus on something moving this quickly is like using a lens designed for a slower world.

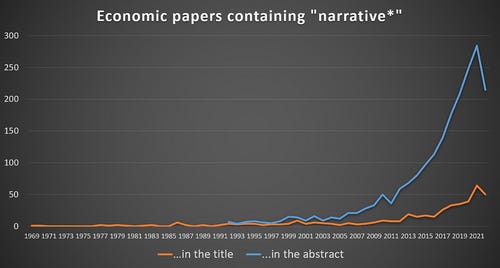

In Narrative Economics, Robert Shiller argued that stories spread like epidemics and move markets in the same way, using the same contagion math as viruses. The dot-com boom, the housing bubble, and the rise of crypto are examples. Narratives did not just describe these bubbles; they caused them. They had their own influence on economic behavior, pushing people to buy, panic, and hold, not because of data but because of stories.

Looking back, that world feels like it has disappeared. Shiller’s narratives spread only as quickly as people could talk to each other. They traveled through dinner parties, newspaper columns, or a coworker mentioning his brother-in-law made money flipping houses in Phoenix. The housing story took ten years to unfold. Bitcoin took years too. People could take time to think about information and decide what to do, which now seems almost old-fashioned.

The whole American lawmaking system acted as a buffer, giving markets time to figure out prices. Policy went through hearings, markups, and floor votes. Markets could process these signals almost in real time, since real time was still measured by people’s pace.

Now, policy appears as a short, capitalized message on a screen. The gap between when something happens and when it is verified has grown.

This change has affected how things work. When policy moved through institutions, the policy itself was the signal. Now, as policy spreads through algorithmic feeds, the headline becomes the signal. The real details come later, after money has already moved. By then, the market’s reaction has become the reality people use to judge the policy.

The headline does not just describe what happened. It becomes the event itself.

This is what headline economics reveals: markets do not trade based on whether a claim is true. They trade on how easily a claim can be turned into a position, how clear its direction is, and how widely it spreads. Tradability is just the starting point. What really matters is whether the headline’s effect on price is big enough to turn voluntary trades into forced ones. Every leveraged position has a breaking point, like a margin level, a volatility target, or a stop-loss, where the holder stops choosing and starts being forced. When a headline pushes the price past that point, selling is no longer a choice but a reaction. In these fast-moving markets, forced reactions are priced in first, and the truth comes later. The main question is not whether the move is correct, but whether it was big enough to trigger the system.

Citrini’s post was tradable because it named specific companies, put them on different sides of an argument, and was clear enough to spread fast. In headline economics, truth comes second. Tradability comes first. The market does not ask if ‘this is real’? It asks ‘can I act on it before someone else does”’

Three decades before Shiller, Soros described a process that, once named, seems obvious, like many destabilizing observations. He called it reflexivity. Markets don’t just reflect reality; they change reality by trying to reflect it, much like describing a marriage changes the marriage, or watching a child changes the child’s behavior. He broke the loop into two parts. The cognitive function is how participants try to understand the world. The manipulative function is how their trades, based on that understanding, reshape the world they’re trying to understand. Your model shapes your position. Your position moves the price. The new price makes your model outdated. You’re never just observing the thing; you’re observing the thing plus your observation of it.

Soros broke the Bank of England by betting against a reflexive loop that the British government would not recognize. But his loops take time. They stretch out and develop. He calls them “initially self-reinforcing” until they reach a turning point. There are stages. You can be inside the loop and still know where you stand.

But what happens if you remove time from the process?

When the reflexive loop speeds up to match the speed of headlines, the cognitive function never gets a chance to work. There is no gap between the headline and the trade. The algorithm reads the words and acts before a person can even process what happened. The manipulative function acts instantly, with no time to think or pause.

Soros’s correction mechanism, the moment when perception drifts far enough from reality to reverse the loop, needs time to work. It needs some slack. If you take away that slack, the loop does not unfold in stages; it explodes. By the time anyone starts to think, the manipulative function has already changed the landscape they are trying to understand.

The headline, a fragment of language, stripped of context, traveling at the speed of fiber optics, has become a fundamental unit of economic reality.

Now, the headline is reflexive over minutes, not months or years. The feedback loop still corrects itself, but the correction looks just like the distortion. The surge and the crash happen almost at the same time. The market corrects by blowing up and rebuilding on the remains, and by the time anyone asks if the original signal was real, three new signals have already made the question irrelevant. Each one is louder, harder to check, and already priced in.

The bruise and the flinch

But the headline is never the cause.

In the opening moments of Bugonia, Teddy’s tension surfaces long before any explanation arrives. You can see it in Plemons’s posture as he rides the bus to his warehouse job at Auxolith, clocking in for the company he secretly plots against. After his shift, he descends into his basement, where he has shaved a woman’s head and smeared her with histamine cream, desperate to strip away her supposed alien powers.

The Citrini post didn’t influence billions because of its novelty. Most fund managers had already considered similar scenarios privately, probably in late nights, mulling over the validation of their worst fears. The possibility that AI might succeed but result in catastrophe had already generated widespread anxiety, distributed across their positions and restless pre-market hours, awaiting definition.

The post gave that fear a skeleton. You can’t trade on a vague dread, but once fear takes shape—becomes architectural—it moves markets. The post didn’t create tension; it simply set it alight.

Most headlines have no significant impact. This aspect is often overlooked, as uneventful headlines rarely receive attention. In a stable market, a headline is analogous to a stone dropped into still water: its effects dissipate quickly. In contrast, a headline introduced into a market already experiencing heightened volatility acts as a tuning fork applied to a crystal, amplifying existing tensions.

You can trace the aftershocks like a seismograph, revealing more about the fault line than the quake itself. A debt ceiling standoff rattles markets not because default is imminent, but because it taps into ten years of unspoken dread about fiscal stability, lurking in the background like furniture everyone ignores.

A headline presses where it hurts. The sharpness of the flinch reveals just how deep the bruise runs.

A headline may cause a temporary market distortion, but markets typically self-correct. For instance, the S&P 500 reached its lowest point in March, 2020, during the height of COVID-19 panic, yet recovered to pre-pandemic levels within months, well before vaccines or economic reopening. Collective market intelligence, informed by millions of positions, models, and intuitions, identified the underlying signal amid widespread FUD. Similarly, the effects of tariff fluctuations diminished over time. Over several weeks, fundamental value reasserted itself, analogous to a house after fire, the temperature may have returned to normal, but the house is gone.

But the path to correction isn’t free.

Markets operate on two levels, each governed by different principles.

The first level is informational. When a headline is released, the market adjusts its pricing accordingly; if the information is later disproven, the market readjusts. This process is rapid, knowledge-based, and largely reversible.

The second level is mechanical and fundamentally different from the first. When a hedge fund reaches its margin limit, the prime broker liquidates the position. A volatility-targeting fund must reduce risk when realized volatility increases. A retail investor’s stop-loss order may execute at a predetermined price, regardless of current market conditions. When a headline pushes prices past these thresholds, selling becomes automatic rather than discretionary. These mechanisms do not evaluate the validity of the underlying signal.

In a world built on leverage, a twelve-minute mispricing can redraw the map of who owns what. A margin call sparked by fiction does not vanish when the story is debunked. The retail investor who panic-sold her 401(k) missed the August rebound—she was already sidelined, her loss sealed by the market’s delayed wisdom. Stop losses snapped shut during Walter Bloomberg’s twelve minutes, draining real money on a phantom signal. The Salesforce PM earning $180k, laid off in a wave of fear, does not get her job back when calm returns. Now she drives for Uber. The price bounced back. Her life did not.

If a headline shock triggers forced selling, and that liquidation hits binding constraints—margin, collateral haircuts, risk budgets, vol targets, then the temporary distortion becomes a state change. Prices can revert to the mean. Capital allocations often can’t.

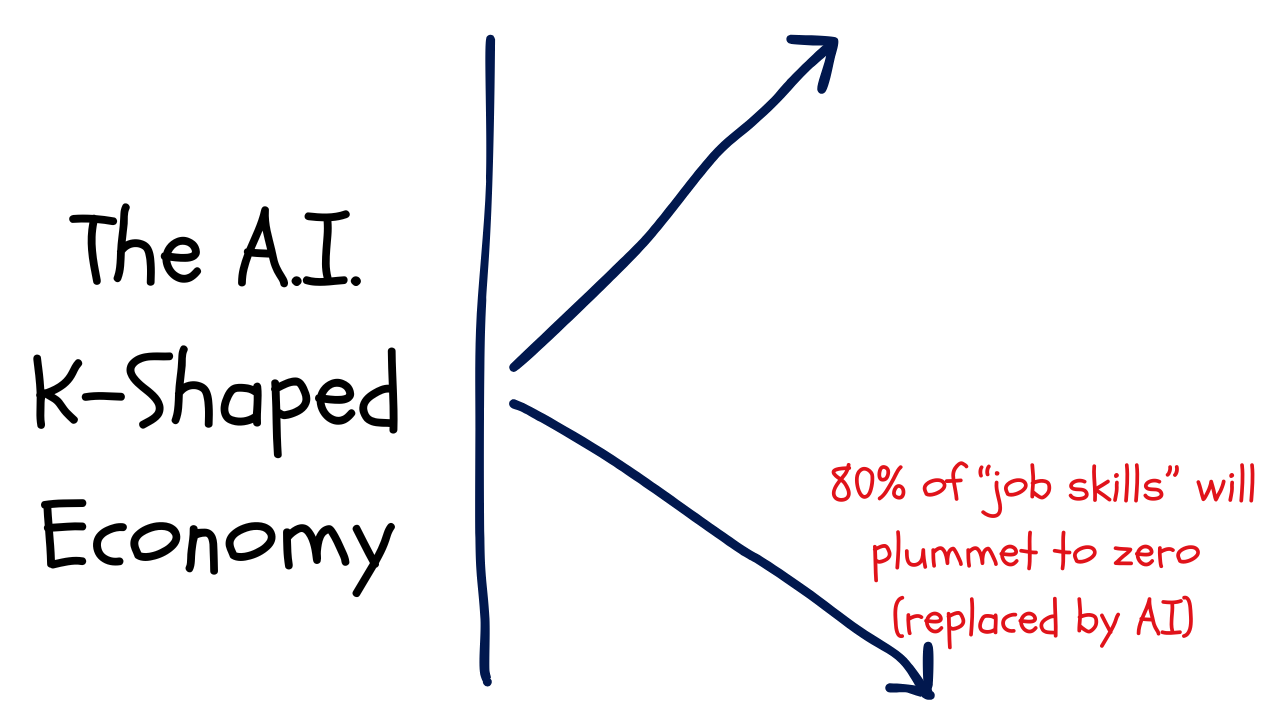

K-shaped economy and K-shaped perception

The damage does not fall equally.

In a so-called K-shaped economy, the bottom half of America, about 165 million people, owns just 2.5% of the nation’s wealth. Meanwhile, the top 10% controls 87% of the stock market. Since ChatGPT appeared, AI stocks have driven three-quarters of S&P returns. Half the economy is powered by a small group, riding a wave that most Americans never joined.

The fund manager who panics out of ServiceNow on Monday morning is the same fund manager who rotates into Micron on Monday afternoon.The Citrini post was bearish for software and payments but wildly, almost giddily bullish for AI infrastructure. If you had the stomach to read it that way.

At the top, where participants wield the manipulative function, a headline is a trade. Reading the Citrini post becomes the trade. The words spark fear, the fear triggers the sell, the sell makes the Bloomberg headline, the headline breeds more fear, more selling. Cognition and action fuse. The portfolio rebalances before the second cup of coffee cools.

At the bottom, you have the cognitive function and nothing else. You read the same post. You feel the same dread. The Salesforce product manager making 180k who gets laid off and ends up driving Uber for $45k a year. The 760-FICO borrowers in SF who did everything right, watching the ground shift beneath mortgages that were good on the day they were written. You feel all of it. The emotional amplitude is identical to what the fund manager feels, but the economic amplitude is miniscule in comparison.

You can’t pivot. Your RSUs aren’t vested, or they’re so deep in the red you’re paralyzed. You can’t hedge. You can’t short the names you know are doomed. You can’t rotate into Micron. You don’t have a Micron position. You have a mortgage. Your fear has nowhere to go except sharing the post, bookmarking it, arguing on X, texting a friend ‘we’re SO fucked!!!!’

The top’s loop moves markets. Conviction deepens, capital flows, semi stocks rise, and the rising confirms the conviction. But the conviction is threaded with terror that the same thesis that makes you rich makes the world more volatile, and the volatility means your position can reverse in minutes on a post by the 19-year-old day trader named BongLord420 on Reddit. So you trade faster. React harder. Check the feed before the coffee. The greed and the fear compound each other, and the compounding is the volatility, and the volatility is what makes the next headline land harder than the last.

The bottom’s loop moves the feed. Despair deepens, engagement rises, the algorithm shows you more evidence the system is broken. Your feed confirms the feeling. The feeling confirms the withdrawal. The withdrawal steepens the K. Nobody designed this to trap you. It trapped you because trapping you is profitable.

One loop reprices the economy. The other monetizes the emotional wake.

And the algorithm connects them. Engagement peaks at the poles of fear and greed. The poles produce volatility. Volatility produces headlines. Headlines produce engagement.

The algo doesn’t care about truth. It cares about arousal.

Arousal and volatility are the same signal measured in different units.

Each headline lands harder than the last. The system learns its own resonant frequency. Each event enables the next. The precedents don’t merely precede. They compound.

The K-shape isn’t just a result of headline-driven economics; it’s also what makes it possible.

The top is simultaneously terrified of missing the upside and of being caught in the downside. The bottom is simultaneously desperate for explanation and locked out of action. Both are feeding the system that feeds on them.

The market doesn’t merely mirror reality, it conjures reality out of necessity. The K-shaped divide doesn’t just produce different outcomes. It produces different needs for narrative. And those needs are so structurally opposed that they generate irreconcilable worldviews, each internally coherent, each invisible to the other.

Are bees real?

Today, founders, investors, researchers, and anyone with a thesis and an audience are swept into the arena of headline economics.

When the manipulative function required a billion pounds and the conviction to deploy it against a sovereign government, perception engineering was exclusive to the likes of Soros. When it requires a Substack account and twelve thousand well-chosen words, the threshold has dropped to approximately zero.

Not every tweet shakes the market. But in a world of volatility and algorithmic amplification, any narrative can slip into the reflexive loop, where its impact multiplies beyond the narrator’s reach or foresight.

Citrini published a thought exercise. The algorithm selected it for maximum distribution. The distribution moved billions. The movement became a Bloomberg headline. The headline became the story. What began as harmless sci-fi was devoured by the machine. The loop is indifferent to intentions or disclaimers.

A VC sits across from a founder and evaluates the quality of their inevitability and assigns a number to the story. The number is called a valuation. It is a claim about a future that doesn’t exist yet, and her investment is designed to bring that future into existence, which should retroactively justify the number. The inevitability narrative works because enough people feel lost enough to accept that the future will be delivered by someone who seems certain. The certainty isn’t independent of the despair. It feeds on it.

Sweetness is born from the carcass.

Every previous compression of the reflexive loop eventually forced new architecture. The South Sea Bubble produced the first modern financial regulations. The 1929 crash produced the SEC. 2008 produced Dodd-Frank. Each time, a loop ran until it broke something load-bearing, and the breaking forced the construction of new institutions that reintroduced the deliberative space the previous system had lost.

Our turn to build has not yet come. The loop will keep spinning. The real test is whether tomorrow’s market can make the journey to correction survivable for those caught inside.

Morning arrives. A headline flickers on your screen. Numbers shift. You catch it all before your first sip of coffee.

You can feel the pressure, not the headline’s pressure, but your own. The accumulated burden of everything you’ve been modeling and fearing and not yet acting on. The headline didn’t create the uneasiness, but it made the amorphous tangible.

The market always finds its truth, eventually. The real question is what becomes of you in the waiting. The loop steals time, and time is where thought resides.