The Illusions of Barbell Theory

The middle isn’t dead; it’s just harder to see beneath the glare of extreme outcomes.

A friend recently published her first book. Despite critical praise from her immediate literary circles, her publisher delivered a stark verdict along the lines of having to decide whether to go for the “National Book Award” or for “BookTok.” The literary middle market is dead.

The Barbell theory originated as a portfolio diversification strategy in hedge funds, popularized by Nassim Taleb. So it’s cool to hear it in the zeitgeist. Barbell theory is eating the world (or at least, the timeline). I’d be having a conversation with someone about the return to traditional values. The barbell theory would suggest that you either optimize for the hyper-capitalist, profit-maximizing, “secure-the-bag” Machiavellian, or pure, good-hearted, God-abiding family life. You gotta barbell it.

All of a sudden, the theory seems to have become the dominant metaphysical framework to understand what’s going on. It posits that technological acceleration (e.g., algorithms) and network effects have fundamentally altered the distribution of outcomes across all domains of human achievement. Where bell curves once dominated, describing a world of averages and incremental gains, we now see radical bifurcation: a world splitting into exponential winners and absolute losers, with the middle ground not just shrinking but actively hostile to value creation.

In many ways, barbell theory is the inverted bell curve, just like this diagram by Peter Thiel at his lecture at Stanford.

The metaphor itself is seductive in its simplicity: a weightlifting barbell, with heavy loads at both ends, and a thin connecting bar in between. No weight in the middle. No value in the average. It's a compelling image for our winner-take-all zeitgeist.

This isn't merely about income inequality or market dynamics. The barbell theory has become a kind of secular eschatology, promising salvation through extreme outcomes while condemning the middle path as a form of living death. Tyler Cowen's "Average Is Over," the book that provides some data points to this philosophy, argues that technology will cleave humanity into a cognitive elite who master technological leverage and a vast underclass subsisting on its outputs.

However, the framework, while compelling, confuses a narrative convenience with a law of nature. And even more interestingly, the belief of the presence of the barbell theory reflexively enhances the barbell nature of any situation, even if the outcome of converging to either side of the barbell rationally yields a worse outcome than simply being “average.”

I call this shaded area ‘voluntary loss,’ the opportunity cost we accept when we force a world of nuance into a binary frame, and in doing so, forfeit the steady gains of the middle. Admittedly, this is a reductive abstraction, intended solely to illuminate the underlying principle.

Barbell theory, compelling and pervasive as it is, has begun to shape not just our perceptions but our actions, nudging us inexorably toward its extremes. We chase the alluring ends, convinced that mediocrity or average pursuits carry no expected value, only silent stagnation. NO ONE WANTS TO BE MID.

The barbell’s gravitational pull distorts everything from career choices to patterns of consumption. College graduates toggle between “grinding LeetCode (or cheating) for FAANG” or “getting into YC,” dismissing stable mid-tier opportunities as invisible or irrelevant. Creative professionals oscillate between chasing viral fame and risking obscurity, while the steady, cumulative path of craftsmanship fades from view. Writers face the same false choice my friend encountered: literary prestige or viral BookTok fame, as if building a readership through book clubs, independent bookstores, and word-of-mouth had somehow ceased to exist.

Even consumer preferences seem to be bifurcating: people seek either the curated luxury experience or the no-frills roadside dive, bypassing the everyday reliability of the neighborhood restaurant, the local bookstore, the mid-tier hotel. These casualties of the barbell worldview illustrate how the value of the middle is systematically erased… but is that really our revealed preference?

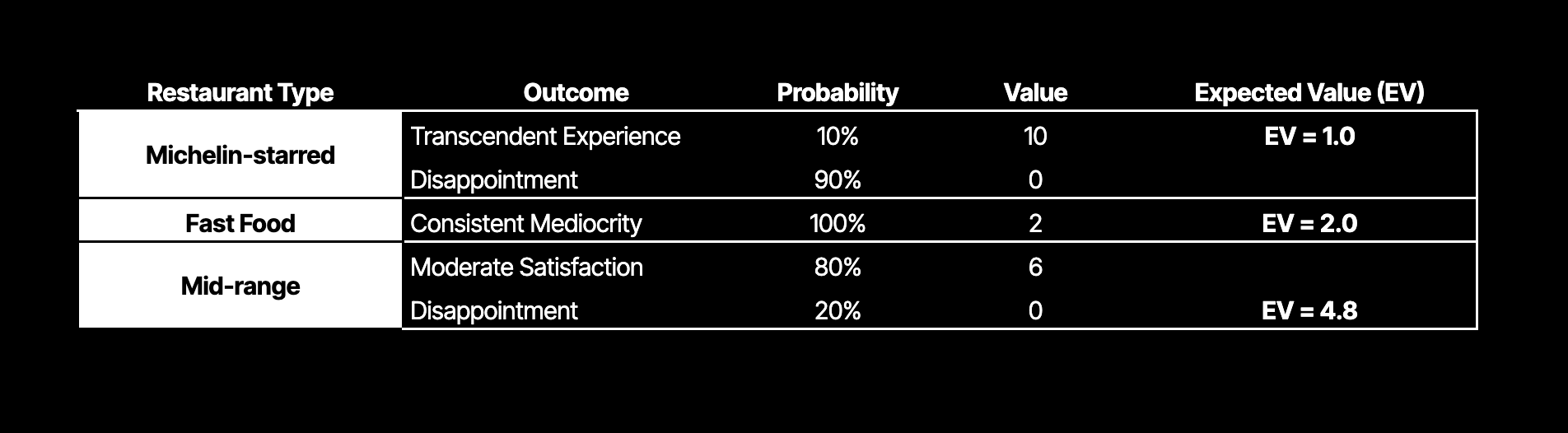

Let’s say we apply the Barbell theory to this somewhat silly example of choosing a restaurant: either a Michelin-starred restaurant or McDonald’s, with nothing in between. It’s probably quite obvious that it’s not always true. Picking a more “normal” restaurant probably wins out in both value and quality compared to either the Michelin-starred option or fast food.

It is worth pausing to delineate the mathematical contours of this difference:

A normal distribution curve represents scenarios where most outcomes cluster around the average, with extreme outcomes becoming increasingly rare. In such a model, incremental improvements yield significant EV because moderate gains are highly probable.

The barbell theory proposes an inverted or bifurcated distribution, where outcomes are concentrated at the extremes, and middle-ground outcomes are comparatively rare or even considered negligible.

Critically, assuming a barbell-shaped reality in situations that more accurately reflect a normal distribution can lead to suboptimal decisions. If moderate success is indeed common and valuable, ignoring it for a slim chance at extremes is mathematically irrational and practically disadvantageous.

In the startup landscape, this distinction is starkly visible. Venture capital's devotion to power-law returns fosters the illusion of binary outcomes. Founders are sometimes compelled to pursue unicorn status or accept oblivion. Yet the practical reality is a bit more nuanced.

In venture, returns cluster at extremes, algorithms drive engagement to poles, and as Peter Thiel notes, founder personalities that seem unhinged in normal life often yield extraordinary outcomes. These power laws are real. But venture capital's outsized cultural influence filtered through TechCrunch headlines and YC playbooks has led to the overgeneralization of what should remain a specialized model. Not every business needs to be a unicorn or a bootstrap. Not every domain follows power law distributions. Yet everyone increasingly feels somewhat pressured to choose between these extremes, as if the middle ground were mathematically forbidden rather than merely unfashionable.

This distortion extends beyond individual choices to our collective decision-making, such as our political discourse. Society increasingly perceives policy debates as stark binaries-socialism versus capitalism, liberty versus control. Yet actual policy outcomes typically conform more closely to normal distributions, with incremental improvements and moderate policies offering meaningful expected value, enhancing overall societal well-being.

Barbell theory is not merely a description of the world; it is an incantation that, once believed, reflexively shapes reality in its image. The more we insist that only extremes matter, the more we engineer systems—investment structures, cultural algorithms, even personal ambitions—that reward only the outliers and starve the center. In this way, the myth becomes self-fulfilling: the middle ground is not lost to entropy, but actively dismantled by our collective refusal to see its worth.

Yet beneath this manufactured scarcity, the middle is not a wasteland of mediocrity but the quiet engine of civilization itself. It is the unglamorous store manager, the midlist novelist, the regional manufacturer—those who persist in the steady work of maintenance and incremental progress. They are the ballast that keeps the ship upright while the spotlight chases the acrobats at either end. The barbell’s true paradox is this: we chase the extremes, but it is the center that endures, adapts, and ultimately sustains the system’s very possibility.

The middle isn't dead; it's just harder to see beneath the glare of extreme outcomes.

Perhaps barbell thinking is itself a historical anomaly, the intellectual artifact of a very specific moment in time. The venture boom of the 2010s, fueled by zero interest rates and platform monopolies, created a generation that mistakes temporary conditions for eternal truths. When money was free and winner-take-all dynamics seemed inevitable, extreme outcomes appeared to be the only rational strategy.

But what happens when the underlying conditions shift? When interest rates rise and capital becomes expensive again? When does antitrust action fragment platform monopolies? Network effects and attention capture endure, but their contours shift. Influence pools in unexpected corners. New gatekeepers emerge—platforms, personalities, algorithms—redrawing the boundaries of power. The barbell world was built on a foundation of cheap money, amplifying specific types of network effects. As those financial conditions change, the same underlying forces may reward different strategies.

The evidence points in two directions. We may be witnessing a permanent structural shift, where technology has irreversibly concentrated power and returns. We can also believe that we’re in a particular phase of a longer cycle. The post-war boom of suburban businesses, regional newspapers, and mid-market companies was once considered the "golden age" of moderate success, coinciding with regulated markets and geographically constrained competition. The current barbell era emerged when global digital networks removed those constraints. But regulation and competition patterns are already shifting again.

What is certain is that the assumption that moderation equals mediocrity is historically false. Warren Buffett did not build his empire through reckless moonshots, but through the patient, almost monastic ritual of capital allocation. Sam Walton created the world's largest retailer by perfecting the unglamorous middle market, store by store. These weren't small ambitions executed moderately, but massive ambitions executed with methodical discipline.

The founders building quietly profitable businesses today may not be missing the future. They may be building it. They built their empires one customer, one store, one reader at a time, the same steady accumulation that publishers now tell authors no longer exists.