The Spectacle of “Building”

What’s really at stake is not some tired “hard tech versus soft tech” or “state versus market” dichotomy, but the way both systems turn collective delusion into fuel.

Last week, I came across a confessionary note on the app RedNote, the Chinese equivalent of Instagram and Pinterest. The post was written by an anonymous Chinese VC, whose perspectives were honest, resonant, and refreshing, standing out in a pool of vapid content.

I thought it was so great that I decided to translate the post.

A screenshot of the original post

Translation

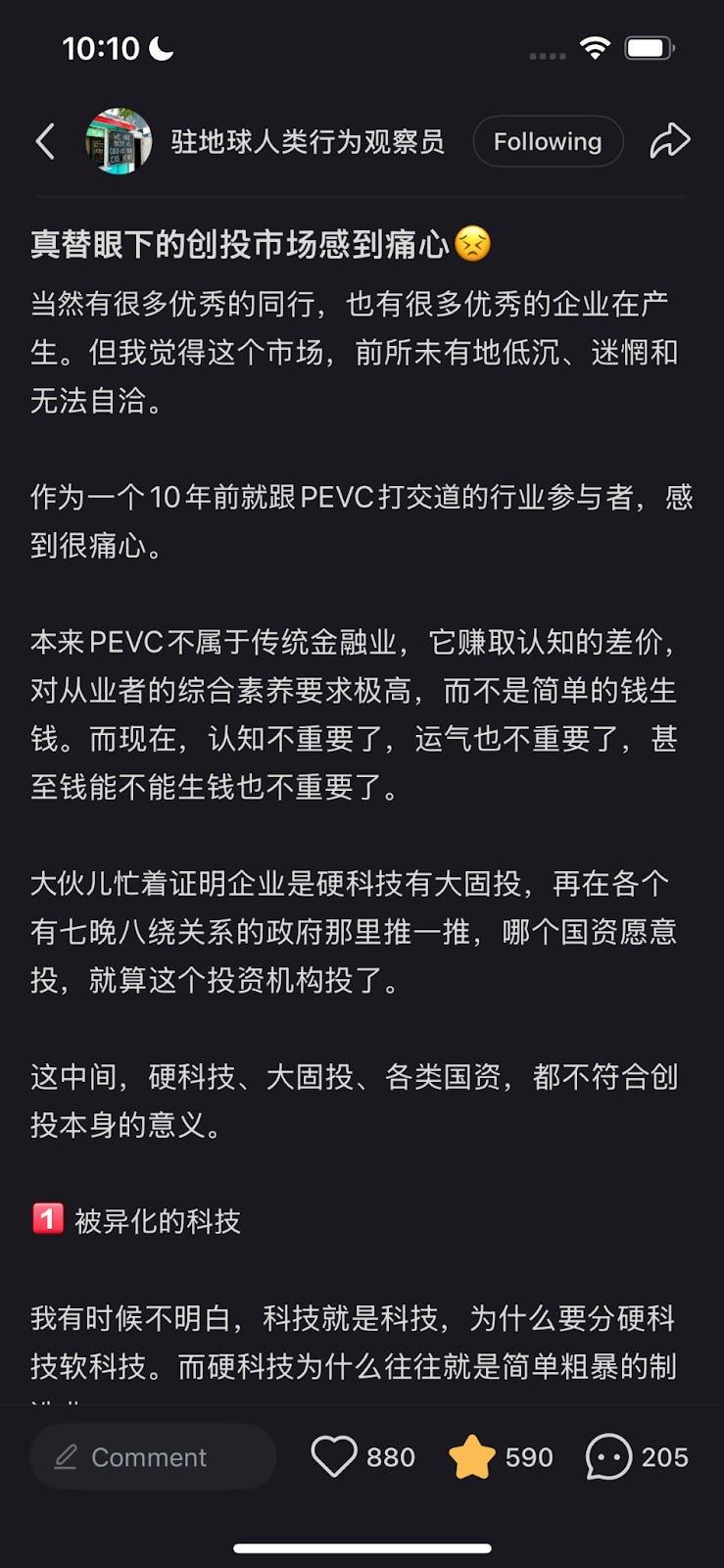

Title: "The VC market under my eyes feels heartbreaking 😣"

Of course, many outstanding peers and many excellent companies are emerging. Yet, this market is unprecedentedly subdued, disoriented, and internally inconsistent.

As someone who's been interacting with private equity and venture capital for a decade, I find this deeply disheartening.

Originally, PE and VC were not part of traditional finance—they capitalized on intellectual arbitrage, demanding extremely high comprehensive qualities from practitioners, far beyond mere capital multiplication. But now, intellect doesn't matter, luck doesn't matter, and even the basic notion of money making more money feels irrelevant.

Everyone is busy proving that companies are engaged in "hard tech" with substantial fixed investments, then navigating complex relationships with various government bodies. If a state-owned entity decides to invest, the investment firm follows suit.

In this scenario, "hard tech," large fixed investments, and various forms of state-owned capital all deviate from the original essence of venture capital.

Alienated Technology

Sometimes I wonder if we've confused weight for significance. Why do we equate ‘hard tech’ with heavy machinery, as if real innovation must be physically massive?

Manufacturing is undoubtedly crucial, but investing in manufacturing for the sake of manufacturing alone often leads professionals to overlook financial models.

Moreover, for quite some time, startups founded by scientists have been highly sought after, as the term "scientist" is easily associated with "technology." Yet, ventures led by scientists often end in chaos.

Forced Fixed Investments

Typically, investors (even those buying stocks) prefer companies with lighter assets, especially during economic downturns when cash itself is scarce, and fixed assets sit depreciating. Now, however, fixed investment has become a rigid evaluation standard, mainly because active funds are mostly government-backed industry funds. Entrepreneurs, in their desperation for financing, artificially inflate their fixed investment requirements. Some might present staged investment plans, while others might even fabricate the amounts spent on fixed assets.

Open Relationships among State-Owned Capital and General Partners (GPs)

Nowadays, it's common practice first to identify a project and then seek state-owned capital. State-owned entities often collaborate simultaneously with multiple General Partners, and GPs may present the same project to multiple state-owned entities at the same time. Many GPs have become mere intermediaries—simple matchmakers.

Due to poor market conditions, it's initially difficult to distinguish between truly professional investors and mere intermediaries. Sometimes, these intermediary-type investors, adept at exaggeration and flattery, are even more popular than professional investors.

What pains me most is seeing how those who pursue quick gains (looking for immediate profits) often succeed more easily than those with true professionalism, whether among state-owned entities, entrepreneurs, or investors.

I've even received three different business plans from the same company, each with entirely different valuations, funding needs, and paths to going public, each tailored for different types of investment firms.

Ah, truly disheartening.

Even the two most iconic figures in the Chinese venture capital market have long since left the country.

China's venture capital landscape has undergone a significant shift, with government guidance funds (GGFs) now dominating and a growing focus on "hard tech" following a tech crackdown. Private deal volume and value significantly dropped between 2022 and 2023. Traditional innovation sectors, such as consumer social, education, and gaming, have declined, giving way to advanced manufacturing and fields like artificial intelligence. The government has implemented measures to address issues with guidance funds, forcing Chinese VCs to prioritize national goals over market opportunities, thereby reshaping China’s innovation ecosystem.

The confession is a warning of innovation degenerating into spectacle, where optics eclipses substance. Investors become matchmakers, companies present tailored narratives, and "hard tech" is idolized regardless of viability, symptoms marking the late stage of the “spectacle of building.”

The spectacle of “building" describes systems that optimize for whatever can be ritualized, narrated, and scaled. The argument isn’t that spectacle alone is negative. Quite the opposite. Byrne Hobart and Tobias Huber, in their recent book Boom, make the persuasive case that bubbles aren't merely collective irrationality; they’re crucial for innovation. Bubbles draw in the capital, attention, and human energy needed to chase ambitious, improbable ideas.

Most ventures fueled by these bubbles implode dramatically. But at the scale of entire ecosystems, this frenzy of experimentation accelerates discovery, pruning countless bad ideas while swiftly elevating the few that truly matter. Without speculative exuberance, railroads, the internet, or even AI might never have reached escape velocity.

The crucial difference isn't whether spectacle exists, but how quickly and openly these collective delusions respond when reality reasserts itself.

With the new administration in America, we're also seeing a shift in the narrative towards "building." As someone who self-identifies as a hopeless techoptimist, I'm deeply aligned with the desire to build and to innovate.

For some reason, when I came across this post titled "it's time to publish build", or rather, the prevalent sentiment it represents in the current cultural cycle of technology, I couldn’t help but think of the above confessionary note from that anonymous Chinese VC.

I grew up in a Metropolitan city in China, and my childhood apartment was located in the central business district, where some of the most innovative businesses set up their headquarters or stores. During the Chinese consumer Internet bubbles, rows of yellow scooters and bikes lined up under the old pine trees, and dozens of ride-share companies with their multi-color cars raced through the streets.

There were automated gyms, manless supermarkets, and robotic package pick-up and delivery drop-off kiosks. All of these, in the past years, have now been replaced by floor-to-ceiling glass-paneled EV stores reminiscent of an Apple store. They're all beautiful, gigantic, and new. On one street, we can find four various luxury EV brands with their showrooms.

The sensation is surreal: an urban landscape that is neither post-apocalyptic nor utopian, but something in between. Gleaming towers and elegant showrooms, yet overlaid on the fading scaffolding of yesterday’s hype cycles. The visible churn of capital, ambition, and state planning has delivered a kind of surface modernity, but left a deeper ambiguity about what is being built and for whom. Industrial spectacles have upstaged the consumer internet’s improvisational energy.

In China’s innovation economy, the evidence of progress is everywhere, but the oxygen for genuine experimentation feels scarce. We see the stifling consequences mentioned in that confession:

Investment now deprioritizes analytical rigor and intellectual arbitrage.

Overemphasis on “hard tech” disregards genuine commercial viability.

Asset-heavy investments inflated by state demands unnecessarily burden enterprises.

Investors become mere matchmakers, diluting investment integrity.

Short-term profit incentives foster inconsistency and ethical erosion, hindering sustainable growth.

What’s really at stake is not some tired “hard tech versus soft tech” or “state versus market” dichotomy, but the way both systems turn collective delusion into fuel, and how the shape of the delusion ultimately determines whether anything real and enduring gets built.

It’s easy to reach for common sense, like decentralized systems are messy but resilient, while centralized ones are sleek but shatter under real stress. But what’s genuinely striking is how, for all their differences, both systems tend to converge in the end, each constructing elaborate performances to sustain collective belief, each inadvertently sanding down the friction that makes actual discovery possible. The symptoms may be presented differently, but the underlying dynamics appear eerily similar. The pathologies rhyme even if the costumes are different.

Recently, I had a conversation with the wonderful Linus Lee about the dual capacity of markets and states: each can create collective delusions, shaping what people believe is possible, valuable, or “real.” He called it “top-down vs. bottom-up delusion,” which I found fitting.

States and markets both create reality distortion fields. Each can whip up their flavor of mass consensus, printing stories that nudge people to believe, build, and occasionally, break the rules of what’s possible. But the shape of the spectacle, and how it collapses or mutates under pressure, remains distinct.

I start to think the greatest threat to innovation isn’t picking the wrong system (state-driven vs. market-driven) but optimizing any system for innovation’s performance rather than its messy, uncertain, and necessary reality.

When innovation becomes purely a spectacle, whether performed for party officials in Beijing or venture capitalists in Silicon Valley, we lose the very conditions that make breakthroughs possible. We trade the messy, uncertain, sometimes embarrassing process of genuine discovery for the clean, certain, and ultimately hollow choreography of progress.

In China and many parts of the world, it’s a top-down spectacle: reality is shaped by quotas, policies, or directives from a ministry or a mayor. There’s a kind of surgical coordination when HQ says “build hard tech,” whole industries reorient, capital sluices into “priority sectors.” Careers rise or fall on how precisely you color inside the prescribed lines. It’s beautiful in its clarity, and terrifying in its inertia. Progress can be forced, but so can fictions. Delusions persist because they’re expensive to puncture. Nobody wants to be the person who says the numbers don’t add up until the reckoning, when, all at once, they don’t.

Meanwhile, markets specialize in bottom-up spectacle. Delusion bubbles up in infinite little pockets—crypto Discords, startup accelerators, Twitter threads that spiral into new movements, garage-scale “consensus hallucinations” that occasionally crystallize into something real. The system corrects: ideas die, memes lose steam, funding in specific sectors evaporates with no sight of liquidity, and the players who bet wrong get reset.

Both top-down and bottom-up systems engineer collective delusions, each propagating myths, whether of omniscient planners or visionary founders. They differ not in creating illusion but in how swiftly and transparently illusions collapse.

The myth of the lone founder is as much a spell as the myth of the central planner. Any nascent sector—city, startup, policy regime—only gets off the ground because enough people are willing to lie a little to themselves and to others, or to believe the impossible, until the prototypes, products, or movements grow sturdy enough to survive contact with reality.

But the scale and repairability of these collective delusions couldn’t be more different. In markets, feedback is relentless and public. Anyone can opt out, money dries up, and the scoreboard is visible to all. You can run dozens of experiments, kill your darling, burn the bridge, start from scratch, and there’s always another lane to merge into.

Market delusions burn out quickly but can be wasteful and chaotic. Top-down systems can sustain focus on long-term goals, but they risk defending failing strategies for too long. Each approach trades different types of resilience against different vulnerabilities.

Top-down, imposed delusions have their own metabolism. Feedback can be sticky and slow, with dissenters shuttled into silence or the truth warehoused “for later.” Systems like these can defend a failing script for years, sometimes decades, but they are not always rigid or inert. The Chinese state, for example, has demonstrated the ability to iterate both policy and industry direction at a breakneck pace. Mandates can shift overnight; priorities are reshuffled according to new geopolitical realities, financial tides, or technological breakthroughs.

Yet flexibility has costs: bureaucratic feedback loops and suppressed dissent mean updated scripts rarely confront underlying truths. Even as new directives and strategies replace the old, a deep inertia can persist: failures and frictions get papered over, and self-preservation takes precedence over uncomfortable recalibration.

So when top-down delusions finally break, the magnitude is often systemic: whole industries, generations, or social contracts left to rot or collapse quietly, sometimes all at once, sometimes in swift, coordinated shudders. The real danger isn’t just stasis, but the way flexibility without genuine bottom-up challenge can mask how long the system has been running on theater rather than truth.

Most critically, the flexibility and “escape hatches” are fundamentally different. A system shaped by markets encourages a hundred parallel stories, even if most wilt. In top-down regimes, there’s only one reality, until suddenly, there isn’t. When the script fails, it fails.

So what matters isn’t just the presence of delusion, but the architecture of error recovery: how quickly can the narrative evolve when the script gets out of sync? Who gets to call the bluff and write the next act? Where is dissent metabolized and made useful, and where is it suffocated into compliance?

This is why discerning the scale and metabolism of a system’s delusion matters. When the spell breaks, robust ecosystems allow pathways for dissent and script-flipping, spaces where truth can be metabolized and new realities quickly emerge. Fragile ones get stuck in denial or scramble for hasty rewrites. Resilience isn’t about preventing delusion, but about how rapidly and transparently a system can surface counter-narratives and rebuild from what’s left, turning collapse into renewal rather than stasis or denial.

The best innovation systems foster productive disillusionment: they create conditions under which delusions inspire action, yet swiftly surface contradictions through open, continuous, and rigorous feedback. Healthy ecosystems cultivate productive skepticism, inviting regular resets without shame or catastrophic consequences.

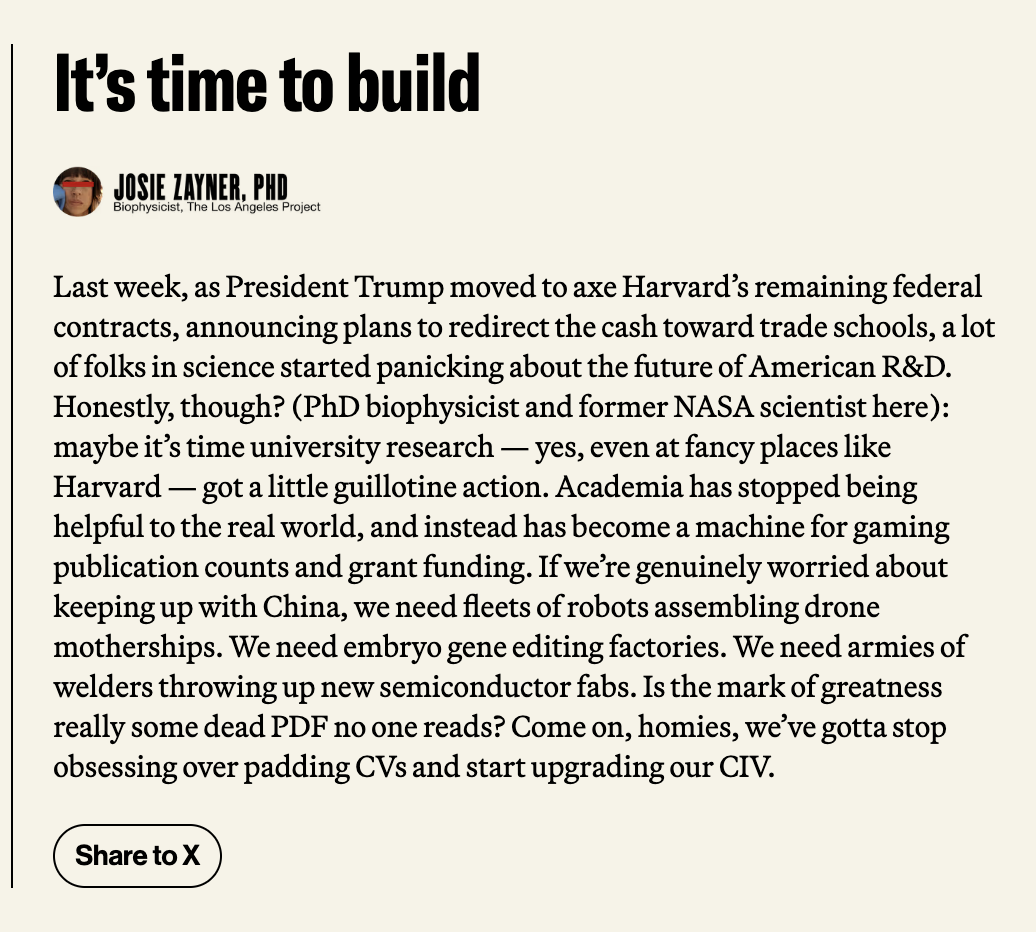

The danger for the West isn't just mimicking China's state-directed approach; it's falling into the false binary of "PDFs versus building." Recent calls to redirect university funding toward trade schools and manufacturing may overlook the fact that the problem isn't that we've too much theoretical work, but that we've lost the conditions for genuine discovery in both theory and practice.

Yes, academic institutions are no longer the origins of the best ideas. Still, what the "PDFs" symbolize, the ability and freedom to propose bold ideas, followed by the will and agency to validate such ideas, still makes innovation possible. The Bitcoin whitepaper is an example, as is the "Attention is all you need" paper. Even a blog post like "Why software is eating the world" has been an empowering call to action for all sectors, not just technology, to reexamine how things can be done and how they can be done better.

The U.S. could maintain such a leading position precisely because of the built-in systematic inefficiency. World-changing breakthroughs and innovations, by definition, cannot follow any predictable patterns and can emerge from anywhere. The real lesson from both the Chinese VC's confession and America's current "building" moment is that breakthrough innovation requires defending the weird, the ambiguous, the half-finished spaces where genuine surprise can emerge.

To build is as much an act of courage as an act of precision. The danger is not in picking the "wrong" model, but in becoming so fixated on signaling compliance, whether with the state, with markets, or with metrics, that we extinguish the subtle, irreducible weirdness from which real progress comes.

The real choice isn’t between "building" and "not building," but between fostering systems that reward actual breakthroughs versus those that merely celebrate their appearance. True innovation thrives in cognitive friction; spectacle eliminates it.

Innovation isn't choreography or theater; it’s dangerous, uncertain, and often irrational, exactly why genuine breakthroughs surprise us. Sometimes, it’s a PDF read by three people that remakes the world. Sometimes, it’s a factory line no one believed in, until it worked.

The only reliable truth: breakthroughs are, by definition, unpredictable. They require room to breathe and room to fail.